Can the IRS Take Your House or Car for Tax Debt? What Taxpayers Need to Know in 2026

If you owe back taxes, you’ve probably heard frightening stories about the IRS seizing your home or car. While the IRSdoes have legal authority to seize property, the reality is far more nuanced. Understanding the process can help you make informed decisions about your situation.

What Authority the IRS Has to Seize Property

A tax lien is a legal claim that secures the government’s interest in your property when you owe taxes. It means the IRS has a right to your property if you don’t pay your tax debt, but it doesn’t mean the IRS is taking anything away from you right now.

A tax levy is when the IRS actually takes (or seizes) your property to collect unpaid tax debt. This can include taking money from your bank accounts, a portion of your wages, or other physical assets you own.

Property seizure, in IRS collections, is when the IRS physically takes things you own, like cars or real estate. The purpose is usually to sell them and use the proceeds to pay your tax debt.

Under Internal Revenue Code Section 6331, the IRS has broad levy authority, but seizing physical assets is only considered after all other approaches have been exhausted.

Can the IRS Take Your House?

Yes, but with major restrictions. IRC Section 6334(e)(1) requires written approval from a U.S. District Court judge before seizing principal residences. The IRS must prove all procedures were followed, the tax is owed, and no reasonable alternatives exist.

Home seizures are extremely rare. For example, in 2021, the IRS issued over 305,000 third-party levies but physically seized property in only 96 cases. Situations where seizures occur usually involve large debts and repeated lack of response, but every case is handled with care.

If you owe $5,000 or less, your primary residence is exempt from seizure under IRC Section 6334(a)(13)(A), though other collection methods may still apply.

Can the IRS Take Your Car or Other Personal Property?

The IRS can seize vehicles and personal property, though rarely. They consider equity, seizure costs versus proceeds, and alternatives. If your car is worth $15,000 but you owe $14,000, minimal equity makes seizure less likely, as the IRS generally considers cost-effectiveness. Business asset seizures need Area Director approval.

The Long Process Before Property Seizure Happens

Seizure does not occur without warning:

Tax Assessment: IRS sends your first bill

Additional Notices: Follow-up letters over weeks/months

Final Notice: Sent 30+ days before levy, triggering CDP hearing rights

Approvals: Manager approval for property; court approval for homes; Area Director for business assets

What Is Protected from IRS Seizure

IRC Section 6334 exempts: necessary clothing and school books; household goods/furniture (up to limits); work tools; unemployment benefits; certain pensions; workers’ compensation; child support; disability payments; public assistance; minimum wages.

Note: Retirement accounts can be levied for flagrant conduct; the IRS can levy 15% of Social Security benefits; state exemptions don’t apply.

What Is Protected from IRS Seizure

Installment Agreement:

Monthly payments over time. Taxpayers owing $50,000 or less may qualify for streamlined online agreements. An approved agreement generally stops collection actions and reduces penalties while you remain in compliance.

Offer in Compromise:

Settle for less than owed. The IRS may accept offers that represent the maximum the agency can reasonably expect to collect. Collection activity is generally suspended during the evaluation period.

Currently Not Collectible:

If the IRS determines that paying would create severe hardship, they may temporarily designate your account as Currently Not Collectible and suspend active collection. Requires Form 433-F/433-A/433-B. Interest and penalties continue.

Appeals:

Collection Due Process hearing (request within 30 days); Collection Appeals Program; Taxpayer Advocate Service.

Common Myths About IRS Property Seizure

Myth: IRS seizes houses without warning.

Reality: Multiple notices required over months, plus court approval for residences.

Myth: Seizures happen frequently.

Reality: Under 100 physical seizures annually.

Myth: IRS can take everything.

Reality: Federal law exempts necessities, work tools, and minimum income.

Myth: Nothing stops seizures.

Reality: Release requests, payment arrangements, and hardship status requests can be submitted at any point, subject to IRS review and approval.

Frequently Asked Questions

Can the IRS really take your house?

Yes, after a court order and no alternatives. Fewer than 100 cases yearly.

How long does a seizure take?

Several months minimum – bills, notices, 30-day Final Notice, approvals.

Can the IRS take your car?

Yes, but rarely. IRS reviews equity, costs, and alternatives.

What happens before a seizure?

Tax assessment, bills, notices, Final Notice 30 days prior, CDP hearing offer, approvals.

Can the IRS really take your house?

Yes, after a court order and no alternatives. Fewer than 100 cases yearly.

Can you stop seizures?

Yes, seizures can potentially be stopped. Options include paying the debt, an installment agreement, demonstrating hardship, or showing that viable alternatives exist. IRS evaluates each case.

What property can’t the IRS take?

IRC 6334 exempts clothing, school books, household goods (limits apply), work tools, unemployment, pensions, workers’ comp, disability, public assistance, and minimum wages.

Will the IRS warn you before taking any action?

Yes. In most cases, the IRS must send bills, notices, and a Final Notice of Intent to Levy, giving you 30 days to respond before taking action. Immediate action without notice happens only in rare cases called jeopardy levies, when the IRS believes collection is at risk.

Property seizures are rare and well-regulated, occurring only after months of notice. The IRS can seize homes or cars as a last resort, with at least 30 days’ notice required by law.

You have rights: CDP hearings, payment plans, offers, hardship status, and appeals. Property protections exist regardless of debt amount.

Ignoring notices moves you toward enforcement. Contact the IRS, consult tax professionals, or reach the Taxpayer Advocate Service.

The IRS has established programs to work with taxpayers making good-faith efforts to resolve their debt. These programs are available – but only if you take action.

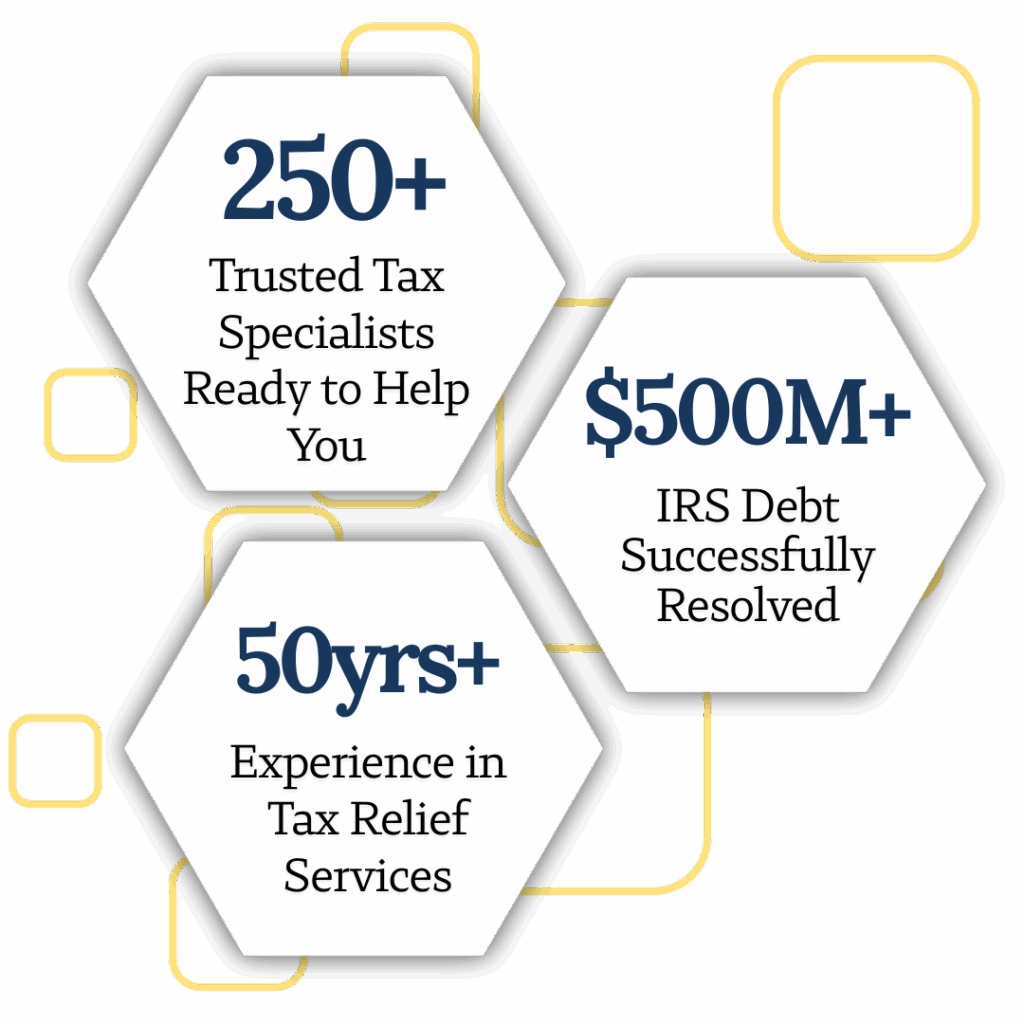

We’re Helping Thousands Of Americans Resolve Their Tax Problems With The IRS. Call 1-888-615-8342 to speak with a tax specialist and explore your options with confidence.

Learn how to check your IRS debt online in 2026. Step-by-step guide to accessing your tax balance, understanding penalties, and exploring payment options.

Learn what happens when you skip filing IRS tax returns for years, including penalties, lost refunds, IRS enforcement actions, and how to fix unfiled taxes.

Learn what happens when you file new taxes while owing IRS debt, how refund offsets work, and which IRS payment or relief options may apply before 2026.

Financial hardship is a tough place to be in and you need all the help you can get so you’re not placed in further debt. Call ACTR now for financial freedom!

Tax professionals are your mediators between the IRS and you. Their sole purpose is to support you and guide you while you negotiate with the IRS together.

The Partial Payment Installment Agreement (PPIA) is a tax relief program designed for individuals with low disposable income and can’t make minimum payments.

There are a few different payment options you may choose from: Short term or long term. Both allow you to pay your tax bill over time. Which one is better?

The information provided in this article is for general informational and educational purposes only and does not constitute legal, tax, or financial advice. This content is not intended to replace professional advice from a qualified tax attorney, certified public accountant (CPA), or enrolled agent.

Tax laws and IRS policies are complex and subject to change, and individual circumstances vary. Any actions taken based on the information contained in this article are done at the reader’s own discretion and risk.

No attorney-client or professional relationship is created by reading or relying on this content. For advice specific to your situation, you should consult a qualified tax professional or legal advisor.

Get Your Tax Resolution Started with a FREE Consultation!