How IRS Tax Liens Affect Homeowners and Property Ownership in 2026

If you own a home and owe back taxes, you may have heard the term “federal tax lien” and felt a jolt of anxiety. What exactly does it mean? Will the IRS take your house? Can you still sell your property? These are reasonable questions -and the answers matter.

This article explains how IRS tax liens work, how they affect homeowners specifically, and what your options are if you’re dealing with one.

What Is an IRS Tax Lien?

A federal tax lien is the government’s legal claim against your property when you neglect or fail to pay a tax debt. According to the IRS, the lien arises automatically once the IRS assesses a tax against you, sends you a bill, and you fail to pay the amount in full.

The IRS may then file a public document called the Notice of Federal Tax Lien(NFTL) to alert creditors that the government has a legal right to your property. This notice is filed in the public record – often with your county recorder’s office – and it covers all your current property, as well as any property you acquire in the future while the lien is active.

Important: A lien is not the same as a seizure. The IRS filing a lien against your home does not mean they will automatically take it from you.

Once a federal tax lien is filed, it attaches to all of your assets – including your home, other real estate, vehicles, securities, and even assets you acquire later. For homeowners, this has some real consequences:

Credit impact. The filing of a Notice of Federal Tax Lien can affect your ability to obtain credit. As of this writing, the three major consumer credit bureaus have generally stopped including federal tax liens on standard consumer credit reports; however, some lenders and specialty reporting agencies may still access lien records through public filings.

Financial flexibility.Lenders and title companies routinely search public records. A filed lien can complicate or block access to new financing.

Duration.The lien generally remains in place for up to 10 years from the date the tax was assessed. In certain circumstances, the IRS can refile the lien to extend its effectiveness beyond that period.

The lien does not change who owns the property, but it creates a legal encumbrance on the property that remains until the underlying tax debt is paid.

How IRS Liens Affect Property Ownership Rights

For homeowners, a federal tax lien most directly impacts three activities:

1. Selling your home. If there is a federal tax lien on your home, the lien will generally need to be addressed – either through payment, discharge, or another IRS-approved process – before or at the time the sale is completed. Normally, if you have sufficient equity, the lien amount is paid out of the proceeds at closing. If the home is being sold for less than the lien amount, you may apply to the IRS for a certificate of discharge. If approved, this removes the lien from that specific property, allowing the sale to move forward. Approval is subject to IRS review and is not guaranteed.

2. Refinancing your mortgage. Lenders require a clear title. A federal tax lien can block or delay refinancing. However, the IRS allows a process called subordination, which does not remove the lien but lets the lender’s interest move ahead of the IRS’s claim – making it possible to refinance or restructure a mortgage.

3. Transferring ownership. Any transfer of ownership of property subject to a federal tax lien may require the lien to be addressed. The IRS has priority over most other creditors once the Notice of Federal Tax Lien is filed.

If you’re trying to sell a property with an active federal tax lien, here is the general process:

Lien with sufficient equity. If the sale price exceeds the lien amount, the tax debt is typically paid at closing from the proceeds, and the sale moves forward.

Short sale scenario. If the home is worth less than what you owe the IRS, you may apply for a certificate of discharge. Whether the IRS approves the application depends on the specific facts and IRS criteria. If approved, the lien is removed from that specific property, but does not eliminate your tax liability – you still owe the remaining balance.

Certificate of Subordination. If a lender needs to be in a superior position to the IRS to issue a loan to a buyer, subordination may be requested.

The key point: you cannot simply transfer a home with a lien and walk away. The IRS’s legal claim must be properly handled before a clean title can be delivered to a buyer.

IRS Tax Liens vs. IRS Levies - Know the Difference

These two terms are often confused, but they represent very different things:

Tax Lien

What it is

A legal claim against property

Effect

Encumbers your property, limits financial options

Automatic?

Arises automatically after unpaid assessment

Tax Levy

What it is

An actual seizure of property

Effect

Takes the property to satisfy the tax debt

Automatic?

Requires additional IRS steps and notice

Tax Lien

Tax Levy

What it is

A legal claim against property

An actual seizure of property

Effect

Encumbers your property, limits financial options

Takes the property to satisfy the tax debt

Automatic?

Arises automatically after unpaid assessment

Requires additional IRS steps and notice

According to the IRS, “A lien secures the government’s interest in your property when you don’t pay your tax debt. A levy actually takes the property to pay the tax debt.”

A lien is a warning signal and a legal safeguard for the government. A levy is the enforcement action. Most homeowners dealing with a lien are not facing immediate seizure of their home, but that can change if the debt remains unresolved.

Yes. When you fail to pay a federal tax debt after the IRS assesses it and sends a demand for payment, a federal tax lien arises automatically and attaches to all your property – including your home.

Does an IRS lien mean the IRS will take my home?

Not automatically. A lien is a legal claim, not a seizure. The IRS would need to pursue a separate action – a levy – to actually seize real property. However, failing to address a lien increases the risk of further collection action.

Can I sell my house if there is an IRS lien?

Generally, the lien must be satisfied before the sale can close. If you have sufficient equity, the tax debt is paid from the sale proceeds. If not, you may apply for a certificate of discharge to allow the sale to proceed.

How long does an IRS tax lien last?

The IRS generally has 10 years from the date of assessment to collect a tax debt. The lien is typically valid for that same period, though the IRS can refile to extend the effectiveness in certain cases.

Can an IRS lien affect my mortgage or my ability to refinance?

Yes. A federal tax lien can block refinancing because it clouds the title. However, the IRS offers a subordination process that may allow a lender to take priority, making refinancing possible.

Does the IRS take the whole property or just the taxpayer’s share?

Generally, the IRS is entitled to levy only the taxpayer’s interest in jointly owned property. In practice, this may require a sale of the asset with the non-liable co-owner receiving their proportionate share.

How can an IRS lien be removed?

By law, the IRS is required to release the lien within 30 days of full payment of the tax debt. In practice, processing times may vary – taxpayers should follow up with the IRS if a release is not received promptly. Other options include withdrawal (removing the public notice under certain conditions), discharge (removing the lien from specific property), and subordination (allowing other creditors to move ahead of the IRS).

Options for Resolving an IRS Tax Lien

The IRS provides several paths to resolve a federal tax lien, depending on your situation:

Pay the debt in full. This is the most direct resolution. By law, the IRS is required to release the lien within 30 days of receiving full payment, though processing times may vary.

Installment Agreement.If you cannot pay in full, an installment agreement allows you to pay over time. In some cases – particularly if you owe $25,000 or less and use a Direct Debit Installment Agreement – you may qualify for a lien withdrawal after meeting certain conditions.

Offer in Compromise (OIC).The IRS’s Offer in Compromise program allows certain taxpayers to resolve their tax debt for less than the full amount owed. Eligibility is based on strict IRS criteria, including income, expenses, asset equity, and ability to pay. The IRS accepts only a portion of OIC applications – not all taxpayers qualify, and the program is not appropriate for everyone.

Discharge. Removes a lien from a specific piece of property, typically used in a property sale.

Subordination. Allows a lender to take priority over the IRS, often used to facilitate refinancing.

Withdrawal. Removes the public Notice of Federal Tax Lien under qualifying circumstances, though the underlying debt may still be owed.

The best strategy depends on your specific financial situation, the amount owed, and what you are trying to accomplish with your property.

Conclusion

An IRS tax lien is a serious matter, but it is not the end of the road for homeowners. A lien is a legal claim against your property, not an immediate seizure. It can affect your ability to sell, refinance, or transfer your home – but there are well-defined IRS processes to work through each of those situations.

The most important takeaway: do not ignore IRS notices. The sooner you engage with the IRS and understand your options, the more choices you will have. Whether through full payment, an installment agreement, an offer in compromise, or a lien discharge, resolving the underlying tax debt is the most reliable path to clearing the lien and restoring full financial flexibility over your property.

For any tax situation involving real property and federal tax debt, consult official IRS guidance at IRS.gov and consider speaking with a licensed tax professional who can help you navigate your specific circumstances.

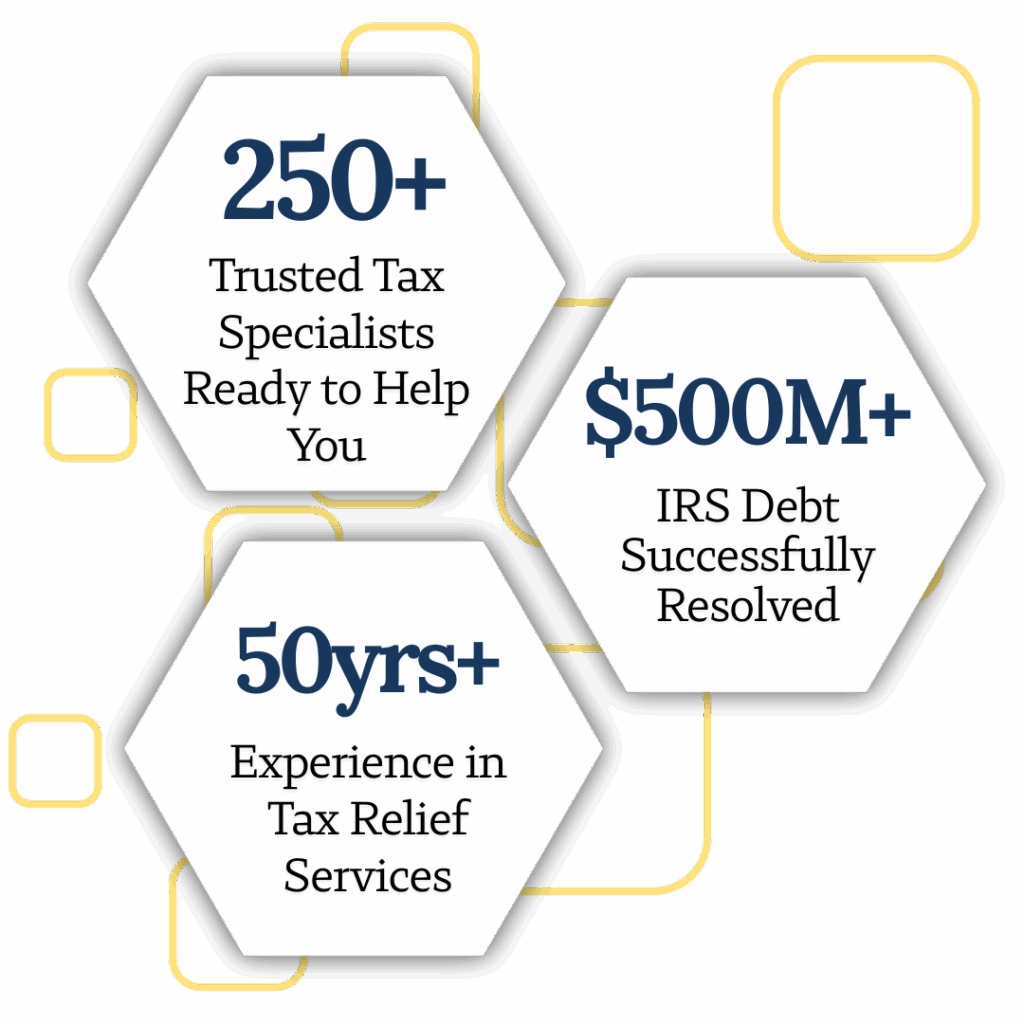

We’re Helping Thousands Of Americans Resolve Their Tax Problems With The IRS. Call 1-888-615-8342 to speak with a tax specialist and explore your options with confidence.

Can bankruptcy eliminate IRS tax debt in 2026? Learn which taxes may qualify for discharge, how Chapter 7 and 13 differ, and what IRS rules you must meet.

Can the IRS take jointly owned property or a joint bank account? Learn your rights, how IRS liens and levies work, and how to protect shared assets in 2026.

Can the IRS take your home or car? Discover what triggers property seizure, legal protections, taxpayer rights, and options to prevent IRS seizures in 2026.

Learn how to check your IRS debt online in 2026. Step-by-step guide to accessing your tax balance, understanding penalties, and exploring payment options.

Learn what happens when you skip filing IRS tax returns for years, including penalties, lost refunds, IRS enforcement actions, and how to fix unfiled taxes.

Learn what happens when you file new taxes while owing IRS debt, how refund offsets work, and which IRS payment or relief options may apply before 2026.

Financial hardship is a tough place to be in and you need all the help you can get so you’re not placed in further debt. Call ACTR now for financial freedom!

Tax professionals are your mediators between the IRS and you. Their sole purpose is to support you and guide you while you negotiate with the IRS together.

The Partial Payment Installment Agreement (PPIA) is a tax relief program designed for individuals with low disposable income and can’t make minimum payments.

The information provided in this article is for general informational and educational purposes only and does not constitute legal, tax, or financial advice. This content is not intended to replace professional advice from a qualified tax attorney, certified public accountant (CPA), or enrolled agent.

Tax laws and IRS policies are complex and subject to change, and individual circumstances vary. Any actions taken based on the information contained in this article are done at the reader’s own discretion and risk.

No attorney-client or professional relationship is created by reading or relying on this content. For advice specific to your situation, you should consult a qualified tax professional or legal advisor.

Get Your Tax Resolution Started with a FREE Consultation!

")