IRS Back Taxes Resolution Guide: How to Resolve Back Taxes in 2026

Owing back taxes is far more common than most people realize. A job loss, medical crisis, business downturn, or missed filing deadline can all leave taxpayers behind. The good news: the IRS has structured resolution options – and understanding them is the first step.

What Are IRS Back Taxes?

“Back taxes” refers to any tax liability not paid by the original due date – whether from unpaid balances, unfiled returns, underreported income, or IRS adjustments. Penalties and interest continue accruing until resolved; interest compounds daily at the federal short-term rate plus 3 percent.

What Happens If You Ignore Back Taxes?

Ignoring a tax debt makes it more expensive. Per IRS Publication 594, the collection process generally follows this sequence:

IRS notices and bills – Including Publication 1, Your Rights as a Taxpayer.

Penalties and interest – continuing to accumulate on the balance owed.

Federal Tax Lien – A public legal claim against your property, including real estate and financial accounts. (IRS: Understanding a Federal Tax Lien)

Levy – Seizure of wages, bank accounts, vehicles, and real estate. (IRS: Levy)

The earlier you engage with the IRS, the more options you have.

Step 1: Determine Exactly What You Owe

The IRS Online Account at IRS.gov lets you view your balance by tax year, review transcripts, identify missing returns, and confirm prior payments – a complete starting point for you and any tax professional.

Step 2: File Any Missing Tax Returns

For most taxpayers with unfiled returns, filing is an important early step – even if you can’t pay immediately. The right approach depends on your circumstances, which a qualified tax professional can help assess.

The failure-to-file penalty is steeper. The IRS charges 5% per month (up to 25%) for not filing, versus 0.5% per month for not paying.

IRS relief programs require filing compliance. Installment agreements, Offers in Compromise, and Currently Not Collectible status generally require all returns to be filed.

Step 3: Explore IRS Resolution Options

The best option depends on your income, assets, expenses, and financial situation.

Installment Agreements allow monthly payments. Short-term plans (within 180 days) do not incur a setup fee. Long-term plans are available for individuals owing $50,000 or less, with up to 10 years to pay. (IRS Topic No. 202)

Offer in Compromise (OIC) settles a tax debt for less than the full amount owed when paying in full would cause financial hardship. The IRS evaluates income, expenses, and asset equity. The application fee is $205 (waived for low-income taxpayers); use the free OIC Pre-Qualifier Tool before applying. (IRS Topic No. 204)

Currently Not Collectible (CNC) Status may be granted when you cannot pay without failing to meet basic living expenses. The IRS generally will not levy assets in CNC status, but interest and penalties continue to accrue. (IRS: Currently Not Collectible)

Penalty Relief is available through First Time Abate (clean three-year compliance history) or Reasonable Cause Relief (illness, natural disaster, or hardship). The IRS generally does not abate interest. (IRS: Administrative Penalty Relief)

Can the IRS forgive back taxes?

Not outright – but an Offer in Compromise may allow settlement for less than the full amount owed, depending on your financial situation.

What if I haven’t filed in years?

The IRS may file a Substitute for Return using available income data, often resulting in a higher bill since deductions are not applied. Filing your own returns – even late – is generally in your best interest.

Can I make monthly payments?

Yes. Individuals owing $50,000 or less can generally apply online for an installment agreement.

Will the IRS take my bank account?

The IRS can levy accounts after proper notice, including a Final Notice of Intent to Levy and Notice of Your Right to a Hearing.

How much do penalties grow over time?

The failure-to-file penalty is generally 5% per month of unpaid tax, up to 25%. The failure-to-pay penalty is 0.5% per month, also up to 25%. In months where both apply, the rates interact – making early action the most effective way to limit total penalties. (IRS Topic No. 653)

Can I settle for less than I owe?

Potentially, through an OIC. Not everyone qualifies, and approval is not guaranteed.

Can the IRS lien my property?

Yes. A federal tax lien arises automatically after an unpaid bill and may be filed publicly, affecting your credit and ability to sell or refinance property.

Can back taxes affect my refund?

Generally, yes. The IRS may apply future refunds to an outstanding balance through the Treasury Offset Program. Certain exceptions may apply.

Common Mistakes Taxpayers Make

Ignoring IRS notices – Each has a deadline; missing them can forfeit appeal rights.

Not filing because you can’t pay – Filing stops the failure-to-file penalty and unlocks payment options.

Missing response deadlines – Collection Due Process hearings require a response within 30 days.

Relying on misinformation – Always verify against official IRS guidance at IRS.gov.

Taking Action: You Don’t Have to Navigate This Alone

The IRS has official resolution programs to help taxpayers address tax debt in a structured way. Engaging proactively rather than waiting gives taxpayers the most options.

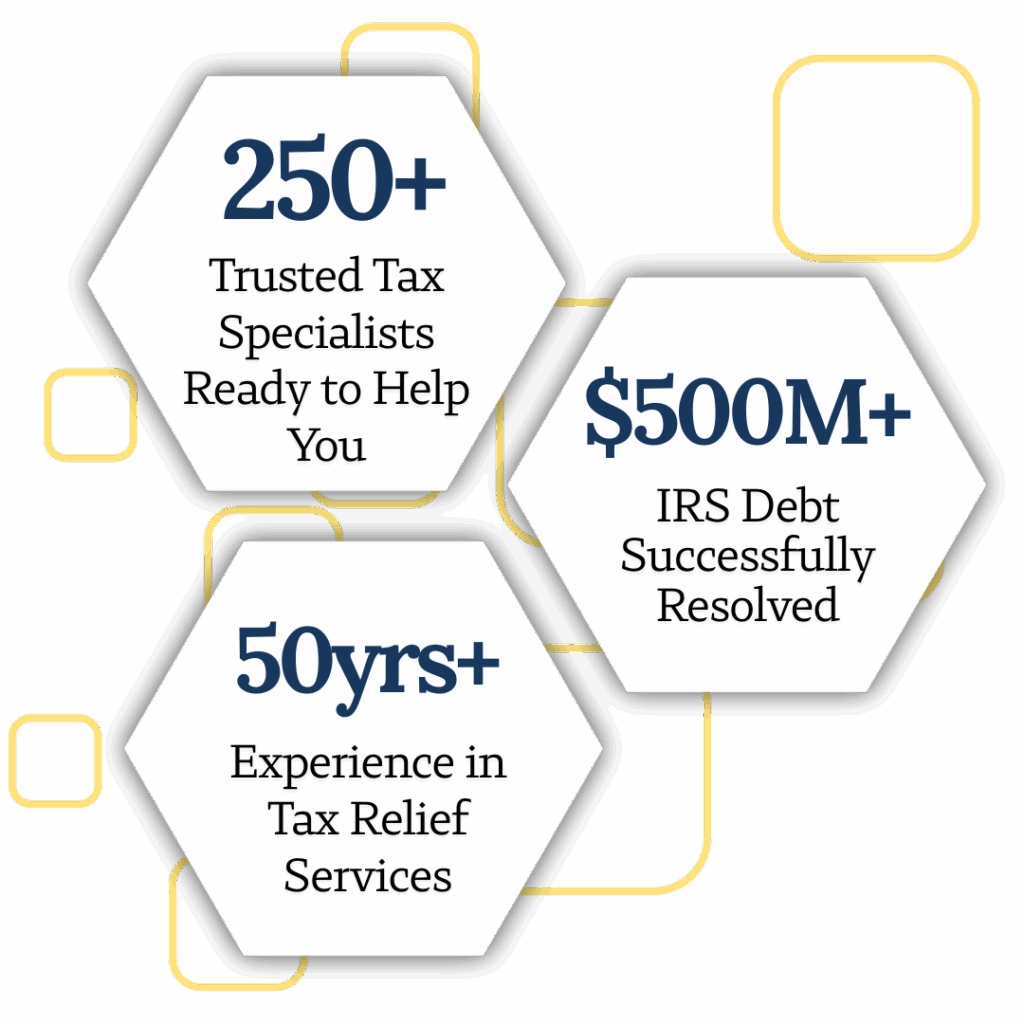

At America’s Choice Tax Relief, we work exclusively with taxpayers facing IRS issues and are here to help you navigate the process clearly and honestly. To talk through your options, we offer a free initial consultation with no commitment required.

Confused about IRS debt? Get clear answers to the most common tax debt questions – from payment plans to liens, levies, and relief options. Know your rights.

Facing IRS debt? Learn how to choose a trustworthy tax relief specialist in 2026 – what to look for, red flags to avoid, and your rights as a taxpayer.

Owe the IRS over $10,000? Learn exactly what happens next – notices, liens, levies, and your payment options – in this step-by-step 2026 guide based on IRS guidance.

Learn the most common tax filing mistakes that trigger IRS letters in 2026 and how to avoid them. Stay compliant with tips based on official IRS guidance.

Received a CP14? Learn what comes next – CP501, CP503, and CP504 explained. Understand the IRS notice timeline and your options before collections escalate.

Got an IRS CP14 notice? Learn what it means, why you received it, and exactly what steps to take next to protect yourself from penalties and further IRS action.

Learn how an IRS tax lien affects your home, property rights, and ability to sell or refinance. Understand your options – based on official IRS guidance.

Can bankruptcy eliminate IRS tax debt in 2026? Learn which taxes may qualify for discharge, how Chapter 7 and 13 differ, and what IRS rules you must meet.

The information provided in this article is for general informational and educational purposes only and does not constitute legal, tax, or financial advice. This content is not intended to replace professional advice from a qualified tax attorney, certified public accountant (CPA), or enrolled agent.

Tax laws and IRS policies are complex and subject to change, and individual circumstances vary. Any actions taken based on the information contained in this article are done at the reader’s own discretion and risk.

No attorney-client or professional relationship is created by reading or relying on this content. For advice specific to your situation, you should consult a qualified tax professional or legal advisor.

Get Your Tax Resolution Started with a FREE Consultation!