Mar. 26, 2026 / Estimated reading time: 10 minutes

IRS Letter CP14: What It Means and What You Should Do Immediately in 2026

Opening your mailbox to find a letter from the IRS can be unsettling – especially when you see the words “balance due.” But before you panic, take a breath. If you’ve received IRS Letter CP14, you’re at an early stageof the IRS collection process – and for most taxpayers, there are still options available. The most important step is acting promptly.

CP14 is the IRS’s first formal notice that you owe money on your taxes. It is not a levy, a lien, or a lawsuit. It is, in plain terms, a bill – and like most bills, it responds well to prompt attention. This article explains exactly what CP14 means, why you received it, and what you should do right now.

What Is IRS Letter CP14?

IRS Letter CP14 is officially known as a Balance Due Notice. According to the IRS, the notice is sent because you owe money on unpaid taxes. It is one of the most common notices the IRS sends, and for most taxpayers it represents the first – and least severe – stage of the IRS collection process.

Your CP14 notice will clearly state:

The total amount you owe, including any penalties and interest that have already accrued

The tax year the balance relates to

The due date for payment

Payment options and instructions for next steps

The notice typically requests payment within 21 days. If balances are owed for multiple tax years, the IRS will generally issue a separate CP14 notice for each year.

The notice typically requests payment within 21 days. If balances are owed for multiple tax years, the IRS will generally issue a separate CP14 notice for each year.

This is an educational illustration based on a CP14 notice is provided to help taxpayers understand the main sections of a typical IRS balance due notice.

*Please note that this is not an official IRS document.

Why You Received a CP14 Notice

There are several common reasons taxpayers receive a CP14:

You filed a return but didn’t pay in full. The most common trigger – you filed your tax return on time, but the balance due wasn’t paid by the deadline. An extension to file is not an extension to pay; the IRS expects payment by the original due date regardless.

The IRS adjusted your return.Sometimes the IRS identifies a discrepancy between what you reported and what third parties (employers, banks, etc.) reported. An adjustment can result in an unexpected balance.

Estimated tax payments were missed or underpaid.Self-employed individuals and others who pay quarterly estimated taxes may receive a CP14 if those payments fell short of what was owed.

It is important to understand that receiving a CP14 does not mean you are in serious trouble or under investigation. At this stage, the IRS is simply notifying you of an outstanding balance.

What CP14 Means for You Right Now

CP14 is the starting point of the IRS’s collection process – not the end. However, it does come with an important time -sensitive element: penalties and interest continue to accumulate on unpaid balances. The IRS states clearly that interest accrues on unpaid amounts after the due date on the notice, and that a late payment penalty applies if you don’t pay in full by that date.

The earlier you act, the less you will ultimately owe. Ignoring the notice won’t make the balance disappear – it will make it grow.

What You Should Do Immediately After Receiving CP14

When you first receive your CP14, take these steps:

Read the notice carefully.The IRS instructs taxpayers to read the notice carefully, as it explains how much you owe and how to pay it. Confirm the tax year, the amount, and the payment deadline.

Compare the amount to your own records. Cross-reference the balance with your filed return and payment history. Check your bank statements or IRS Online Account to confirm whether any payment may already be in transit.

Note the payment due date. The deadline is typically 21 days from the notice date. Mark it clearly.

Keep the notice.You will need the information on it– including the notice number, tax year, and contact phone number – for any further communication with the IRS.

IRS typically contacts taxpayers by mail first. A genuine CP14 will come through the U.S. Postal Service, not via email, text, or phone call demanding immediate payment.

What Happens If You Ignore a CP14 Notice

The IRS does not drop unpaid balances. If you take no action after receiving a CP14, the IRS will proceed through a series of escalating collection notices.If the initial bill goes unpaid, the IRS generally sends a series of notices – CP501, CP503, and CP504 – every few months until the tax liability is resolved.

Here is what that progression looks like:

CP501 ~ 4-6 weeks after CP14

A reminder notice that you still have an unpaid balance, with updated penalties and interest.

While the IRS may send a CP502 as a second reminder notice, it is not always issued. In many cases, the IRS skips this step and proceeds directly to CP503.

CP503 ~ 4-6 weeks after CP501

A second reminder, sent when the IRS has not heard from you; more urgent in tone.

CP504 ~ 4-6 weeks after CP503

A Notice of Intent to Levy. This is a serious escalation. At this stage, the IRS may begin seizing state tax refunds, and further notices – including a final statutory notice – can precede additional levy actions such as wage garnishment or bank account levies.

LT11 / Letter 1058 — Final Notice of Intent to Levy ~ 30 days after CP504

Final Notice of Intent to Levy. This is the final notice before the IRS can take enforcement action.

It also provides your legal right to request a Collection Due Process (CDP) hearing.

Additionally, the IRS may file a Notice of Federal Tax Lien, a public record that can affectyour credit and your ability to sell property.

A Notice of Federal Tax Lien (Letter 3172) is different from a levy. While a levy allows the IRS to seize your assets, a tax lien is a legal claim against your property due to unpaid taxes. The IRS may file a lien at various stages of the collection process, and it can significantly impact your credit and ability to sell or refinance assets.

None of this needs to happen. Acting at the CP14 stage preserves the most options and keeps costs lowest.

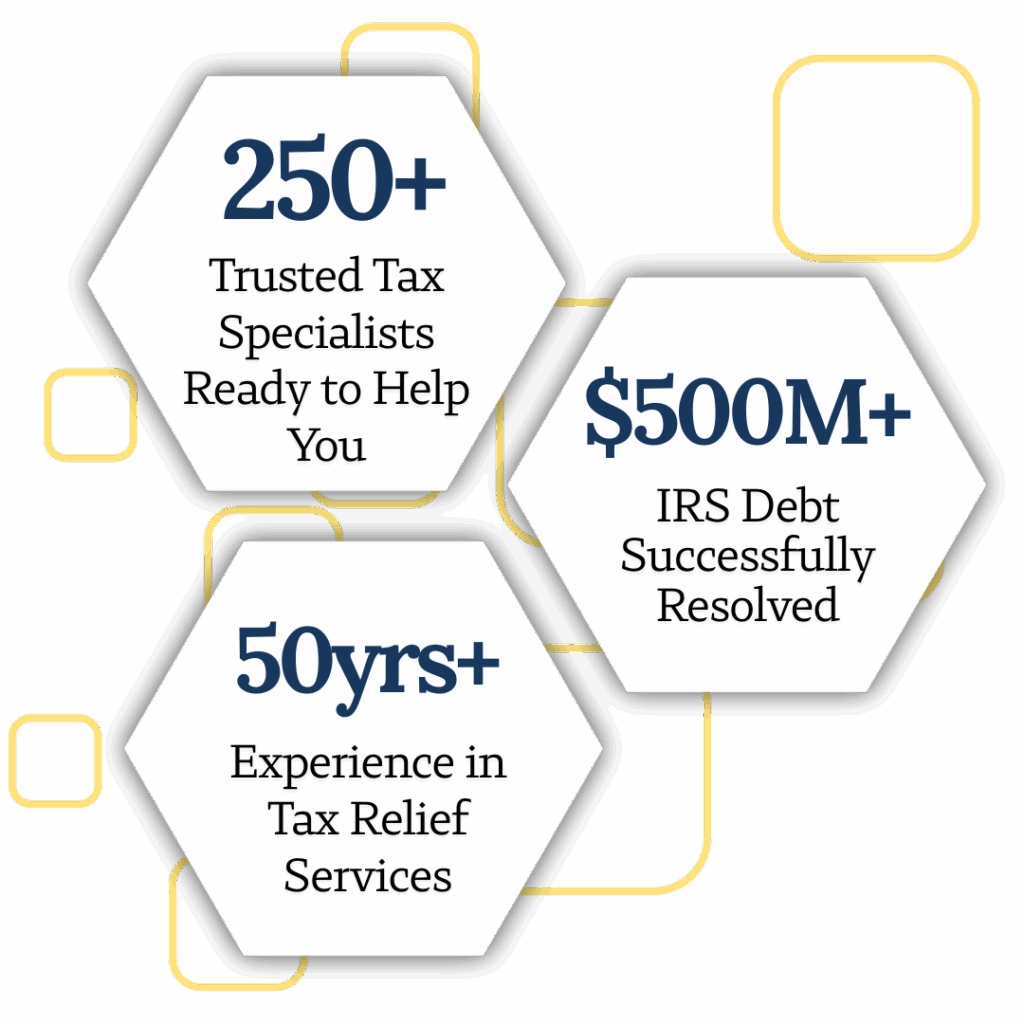

We’re Helping Thousands Of Americans Resolve Their Tax Problems With The IRS. Call 1-888-615-8342 to speak with a tax specialist and explore your options with confidence.

How to Respond to a CP14 Notice

Your response will depend on whether you agree with the balance.

If the amount is correct:

Pay the balance in full by the due date shown on the notice.The IRS offers multiple payment options at IRS.gov/payments, including direct bank transfer, credit or debit card, and check or money order. Paying the full balance by the due date on your notice is the most effective way to prevent further penalties and interest from accruing on that balance.

If you cannot pay the full amount immediately, DO NOT ignore the notice. The IRS offers payment plans (also called installment agreements) that allow you to pay your balance over time. The IRS offers short-term payment plans (up to 180 days) for those who owe less than $100,000, and long-term installment agreements with monthly payments for those who owe $50,000 or less – both available through the IRS’s Online Payment Agreement tool at IRS.gov.

In cases of genuine financial hardship, the IRS may temporarily pause collection efforts, or you may wish to explore whether an Offer in Compromise – a program that allows eligible taxpayers to settle their balance for less than the full amount – could apply to your situation. Eligibility is based on specific financial criteria set by the IRS.

If you believe the amount is wrong:

Contact the IRS at the phone number printed on your CP14 notice. Have documentation ready – such as canceled checks, bank statements, or an amended return. The IRS also notes that if you have paid and believe the notice was sent before your payment was processed, you may not need to take immediate action, but you should verify through your IRS Online Account.

Is CP14 a serious notice?

It is a formal balance due notice that requires attention, but it is not an enforcement action. It is the IRS’s first communication about an unpaid balance. Acting promptly keeps it manageable.

How long do I have to pay after CP14?

The notice typically requests payment within 21 days of the date it is issued. The exact deadline is printed on your notice.

Will the IRS take my assets after CP14?

Not at this stage. Asset seizure (levy) only becomes possible after later notices – particularly CP504 and final levy notices – if no action is taken. CP14 is the beginning of the process, not the end.

What happens if I can’t pay?

You have options. The IRS offers short-term payment plans, long-term installment agreements, temporary collection holds for hardship situations, and Offers in Compromise for eligible taxpayers.

Can I dispute a CP14 notice?

Yes. If you disagree with the balance, call the IRS at the number on your notice and be prepared to provide documentation to support your position.

Is CP14 the first IRS notice?

In most cases, yes. CP14 is typically the first notice the IRS sends regarding an unpaid balance on a tax account. Subsequent notices escalate if no action is taken.

Use Your IRS Online Account

One of the most useful tools available to taxpayers is the IRS Online Account at IRS.gov. Your online account allows you to:

View the amount you currently owe

See your payment history and any scheduled or pending payments.

Review payment plan details.

Access digital copies of select IRS notices.

Setting up or logging into your IRS Online Account can help you verify whether a payment was received, confirm the balance on your CP14 is accurate, and apply for a payment plan – all without waiting on hold.

A note on scams: The IRS will always contact you by mail before calling. If someone calls claiming to be the IRS demanding immediate payment by gift card, wire transfer, or cryptocurrency, that is a SCAM. Verify any IRS communication through your IRS Online Account or by calling the IRS directly at 1-800-829-1040.

Conclusion

For many taxpayers, CP14 represents an early and resolvable stage – but the right response depends on your specific situation, how much is owed, and your filing history. The most important step is acting promptly.

Read your notice, verify the balance, note the deadline, and take action. If you are uncertain about your options or the amount shown, consider reaching out to a qualified tax professional for guidance.

Learn how an IRS tax lien affects your home, property rights, and ability to sell or refinance. Understand your options – based on official IRS guidance.

Can bankruptcy eliminate IRS tax debt in 2026? Learn which taxes may qualify for discharge, how Chapter 7 and 13 differ, and what IRS rules you must meet.

Can the IRS take jointly owned property or a joint bank account? Learn your rights, how IRS liens and levies work, and how to protect shared assets in 2026.

Can the IRS take your home or car? Discover what triggers property seizure, legal protections, taxpayer rights, and options to prevent IRS seizures in 2026.

Learn how to check your IRS debt online in 2026. Step-by-step guide to accessing your tax balance, understanding penalties, and exploring payment options.

Learn what happens when you skip filing IRS tax returns for years, including penalties, lost refunds, IRS enforcement actions, and how to fix unfiled taxes.

Learn what happens when you file new taxes while owing IRS debt, how refund offsets work, and which IRS payment or relief options may apply before 2026.

Financial hardship is a tough place to be in and you need all the help you can get so you’re not placed in further debt. Call ACTR now for financial freedom!

Tax professionals are your mediators between the IRS and you. Their sole purpose is to support you and guide you while you negotiate with the IRS together.

The information provided in this article is for general informational and educational purposes only and does not constitute legal, tax, or financial advice. This content is not intended to replace professional advice from a qualified tax attorney, certified public accountant (CPA), or enrolled agent.

Tax laws and IRS policies are complex and subject to change, and individual circumstances vary. Any actions taken based on the information contained in this article are done at the reader’s own discretion and risk.

No attorney-client or professional relationship is created by reading or relying on this content. For advice specific to your situation, you should consult a qualified tax professional or legal advisor.

Get Your Tax Resolution Started with a FREE Consultation!

")